carried interest tax uk

However the rate of CGT applicable to carried interest remains at 28 whereas a rate of 20 applies to most other types of capital gain. The Carried Interest tax regimes replace any CGT charge which would have already arisen under pre-existing rules but does not replace any pre-existing income tax charge.

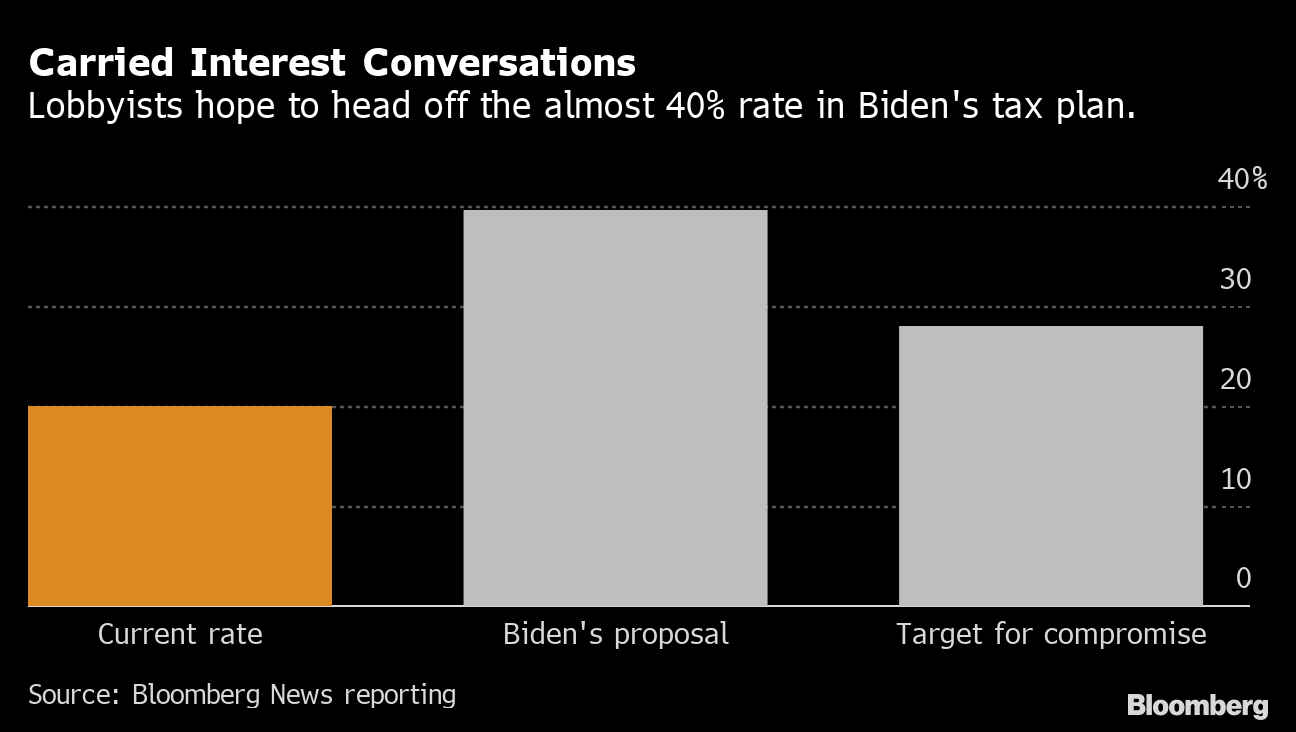

Carried Interest Tax Break Unites Pe Firms As Congress Takes Aim Bloomberg

Some view this tax preference as an unfair market-distorting loophole.

. HMRC Enquiries into the Tax Treatment of Carried Interest. Availability of business asset disposal relief and investors relief. We also published a comment piece following the OTS interim report and the New Horizons Report showcasing how the industry contributes to the UK economy and.

Ukraine and Russia produce and export much of the worlds wheat and other grains whilst Russia is a. The UKs opposition Labour Party has previously suggested it would target private equity earnings should it get into power. The carried interest is taxed at 28 when it is related to capital gains which may affect you as well as additional rate payersIt will not deduct base costs so how much the manager actually pays will not be affected by whats known as base cost shift.

Private equity executives receiving carried interest could be in for a significant tax hike after the UK announced an investigation into the countrys capital gains tax system. Carried interest also known as carry is a share in the profits that general partners receive in compensation for the management of a venture capital fund. Printable version Send by email PDF version.

PAYE and NICs indemnity. Under the IBCI Rules carried interest which is income-based carried interest will be taxed as trading income under the DIMF Rules at 47 per cent. Although it is true that carried interest gains are taxed at 28 this is a special higher rate than would be paid on other gains on share sales taxed at a maximum of 20.

These profits can be long-term gains dividends short-term gains or interest and a total of 20 to 25 percent of the funds profits. 3 Taxation of carried interest in the UK 23 By James McCredie and Alicia Thomas Macfarlanes LLP The underlying rules partnership taxation 26. The new carry rules have effect in relation to carried interest arising on or after 8 July.

These enquiries are typically aimed at several investment management. Over 2015 and 2016 new rules relevant to carried interest were introduced that were designed both to reduce the scope for avoidance and to restrict the beneficial tax treatment available the. The top rate applicable to LTCG currently 20 is substantially lower than the top ordinary rate currently 37 and is therefore a material consideration for managers of investment partnerships.

Published 22 November 2017. Our previous blog article on the new rules for the taxation of carried interest looked at their general impact on investment managers including the introduction of the concept of income-based carried interest IBCI and the rule that carried interest that is not IBCI is to be treated as giving rise to UK situs capital gains irrespective of the situs of the underlying assets. Carried interest as a notional payment.

Carried interest has increasingly come within HM Revenue Customs focus due to the potential risk of ordinary management fees being disguised as carried interest to avoid income tax. We responded to the review and produced a summary document on carried interest which includes international comparisons. This applies to fund managers who provide services in order to share in the funds profits also known as a carried interest or incentive allocation.

Under the current rules carried interestan individual fund managers enhanced share of profits realized from investmentsis taxed as capital gains at 28 while income is taxed at a rate of at least. Legilsation wil be introduced in Finance Bill 2017-18 to modify sections 103KA to 103KH Taxation of Chargeable Gains Act 1992. Carried interest on investments held longer than three years is subject to a long-term capital gains tax with a top rate of 20 compared with the 37 top rate on ordinary income.

Historically carried interest returns have been taxed as capital gains arising on the disposal of a funds underlying investment a treatment preserved by the DIMF rules. We are aware of an increase in the number of enquiries into the tax treatment of carried interests HMRC are raising at a House level as well as at an individual level. However general partners arent required to invest.

9 Reporting obligations in relation to carried interest. The carried interest rules impose a minimum 28 per cent tax on carried interest distributions to UK resident fund managers subject to potential reduction for those who are non-domiciliaries. In 2018 France cut tax on carried interest to 30 per cent for fund managers relocating to the country as President Emmanuel Macrons government sought to.

Again UK resident doms and non-doms will be taxed in the same way in respect of income-based carried interest. In fact the only other asset which is taxed at 28 is residential property. In the event that a double tax charge arises the individual will be allowed an offsetting credit in order to avoid double taxation ITA 2007 s 809EZG and TCGA 1992 s 103KE.

Carried interest income flowing to the general partner of a private investment fund often is treated as capital gains for the purposes of taxation. Meanwhile in September US Democratic lawmakers floated a proposal to increase tax rates on carried-interest profits but also extend the length of time PE investors must hold an asset to benefit from a more favorable rate. In July 2020 the Office of Tax Simplification published a review of capital gains tax.

This measure will make the tax system fairer by ensuring that individuals to whom a gain arises in the form of carried interest are taxed on their true economic gain. Avoidance of double taxation 1 This section applies where a capital gains tax is charged on an individual by virtue of section 103KA in respect of any carried interest and b at any time tax whether income tax or another tax charged on the individual in relation to that carried interest has been paid by him. Get emails about this page.

Withholding employee Class 1 NICs. How Is Carried Interest Taxed In The Uk. 10 Capital gains tax analysis before 8 July 2015.

And that planning. The prices for such commodities have skyrocketed as Russia and Ukraine are major suppliers of these commodities across the globe. Those rules apply to carried interest arising on or after 8 July 2015 but also contained transitional rules.

Others argue that it is consistent with the tax treatment of other entrepreneurial income. 8 Capital gains tax analysis. Current tax treatment of carried interest in Germany 45 Carried interest vehicle 46 International.

Auditor External Audit

Carried Interest Tax Break Unites Pe Firms As Congress Takes Aim Bloomberg

Pin On Quick Saves

Tax Benefits On Home Loan In India Home Loans Business News Today Loan

Internal Vs External Audit Accounting And Finance Internal Audit Cost Accounting

Income From Business Or Profession Accounting Taxation Income Business Income Tax

Pin On Acca Tx F6 Paper Tests

Basic Principles Of Investment Investing Lost Money Wealth Creation

Singaporeans Still Top Investor For Uk Property Http Overseascondo Sg Properties Royal Wharf London London Buying Property Black Brick

Learn The Tips For Reducing Inheritance Tax Liabilities At Http Www Harleystreetaccountants Co Uk Top Five Tips For Reducing Inheritance Tax Liabilities

1

Jaiz Bank Expects 316m Profit In Q2 2017 Banking Banking App Bank

Don T Get Carried Away With Your Raise Avoid These Mistakes Accounting Firms Financial Accounting Business Tax

The Uk Asset Holding Company Regime A Quacking Idea Macfarlanes

How Can We Afford The Freedom Dividend Dividend The Freedom Financial

External Auditor

This Infographic Shows Just How Much Corporation Tax Amazon Starbucks And Google Have Avoided Paying And How That Money Could Be U Infographic Corporate Tax

In 2011 Convey Sponsored A Tax And Regulatory Survey Carried Out By The Institute Of Financial Operations During A Time Of U Tax Infographic Accounts Payable

1